Business Impact

Money for the Masses

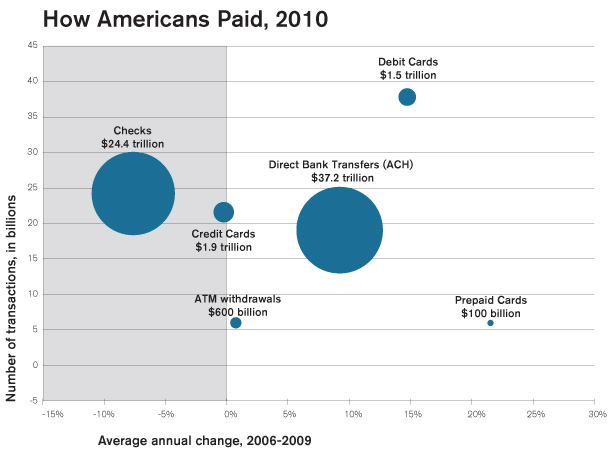

For people who can’t afford a bank account, there’s a prepaid card called Green Dot.

Earlier this month, a Silicon Valley mobile startup called Loopt was acquired for $43 million. Even though Loopt had only a relatively modest user base, it was well known among the tech cognoscenti. But the same wasn’t true of the acquiring company. Who exactly, wondered many writers, was this outfit called “Green Dot”?

In fact, Green Dot is something of an industry giant, an 11-year-old payments company with 4.5 million active customers who used it to complete $16 billion in transactions last year. If it was unknown to many otherwise well-informed tech observers, it’s because the company is targeting a market that, despite its size, is often invisible to the affluent elite whom tech companies usually cater to.

Green Dot is the biggest example of a new breed of financial-services company that aims extremely sophisticated technology at what might seem like a singularly unpromising demographic: the estimated 60 million American considered “underbanked.” Some of these millions subsist at poverty level; many others simply can’t afford the increasingly stiff monthly charges associated with traditional checking accounts.

Currently, many of the underbanked are forced to rely on a demimonde of check-cashing and payday advance services. Journalist Gary Rivlin, who chronicled the financial services aimed at poor people in his book Broke USA, says these services are extremely expensive: many regular check-cashing customers pay $1,000 or more in fees every year.

Green Dot’s product is a prepaid debit card. It looks and acts just like regular Visa or MasterCard plastic, but it must be funded by the owner before it can be used. There is no credit, so there is no way to bounce a check, much less get buried with high-interest credit card debt via impulse purchases.

A Green Dot card costs $4.95 to buy and $5.95 a month to use, though those fees are waived if the card is bought online and used at least 30 times a month. Putting money on a card through direct deposit is free, but it costs $4.95 to load the card in person. The company says the average customer spends less than $7 a month on charges.

While prepaid debit cards are becoming increasingly popular even for traditional banks, Green Dot stands out because it has built a huge retail network of nearly 50,000 locations, including 7-Eleven, Kmart, and Walgreens stores.

Consumer advocates are usually enthusiastic about prepaid debit cards, if only because they don’t give consumers the chance to get into credit trouble. “I like prepaid debit cards, and I like Green Dot,” says Adam Rust, an analyst with Reinvestment Partners, an advocacy group in Durham, North Carolina, that is often critical of financial institutions. “I think they are one of the good guys.” By contrast, Rust says, some other prepaid debit cards come with a long list of hidden fees.

Green Dot, headquartered outside Los Angeles, was founded in 1999 by Steve Streit, a former radio industry executive, who originally aimed the service at teenage shoppers. It grew significantly enough to go public in 2010. Its stock was recently trading near $25, nearly $40 less than its all-time high; financial analysts following the company say Wall Street is worried about turnover, or “churn,” among Green Dot customers.

One customer who has no intention of dropping the card is Molly Ibietatorremendia, a Sacramento mother of three whose husband is a prison guard. What drove them to prepaid cards, she said, was the stiff overdraft charges they were incurring on their occasional inadvertently bounced checks. “We went over a few times and ended up paying $30 even for a 30-cent overdraft,” she says. “We just got tired of it.”

The fact that Green Dot might be aimed at low incomes does not mean it is low-tech. The system integrates with the Visa and MasterCard payment networks, among the most complicated around. The company also had to design and implement a retail card reloading system that was both secure enough to handle huge sums of money and inexpensive enough to roll out in tens of thousands of storefronts. “We had to build quite an extensive technology platform,” says Secil Baysal, general manager of the company’s network.

While its origins are in the unglamorous world of prepaid debit cards, the company is also exploring more distant frontiers of the payment industry. Its Loopt purchase, for example, represents an effort to establish a beachhead in the booming but competitive field of mobile-phone payments. The company promises, though, that any future endeavors won’t change its basic philosophy of going after customers many other companies choose to ignore.