Business Impact

How to Hedge Against Volatile Energy Prices

Businesses of any size can reduce their risks by locking in rates ahead of time.

No matter what product a business sells, one of its costs is energy. And few commodities are as volatile.

“The energy cost will affect whether a product is economical to produce and sell or not,” says Ken Irvin, a partner in the New York law firm Cadwalader, Wickersham & Taft, who advises corporate clients on how to hedge their energy risks and guard against that volatility.

The basic idea behind a hedge is that a company signs a contract to buy some portion of a commodity at a set price. That pays off if prices rise, but it could be a money-losing proposition if they fall below the contracted level. A few years ago, when Southwest Airlines hedged the price of jet fuel, the strategy kept it profitable while other airlines lost money; but when fuel prices later fell, Southwest found itself overpaying. Hedging is available to any company, and at any level that makes sense. Even individual homeowners can sign fixed-price contracts. But Irvin says it’s probably not worth a company’s effort to come up with an energy hedging strategy unless energy is among the top three to five costs in its budget.

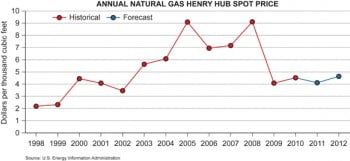

Deciding which future costs to lock in and when is no easy task, says Bill Brewer, vice president for sourcing and sustainability at Summit Energy, a Kentucky-based company that provides energy management services to companies. For instance, which price fluctuations are most relevant to a company’s operations? Electricity might be its biggest energy source, but natural-gas prices can often be more volatile, fluctuating 40 percent over the course of a year, so a company might want to focus more on that. And factories or other facilities have access to different kinds of energy depending on where they’re located. States also have different rules about who can sell energy and how; some mandate that utilities buy back energy from third parties that produce some of their own, a requirement that can affect local prices. Sometimes it might make sense to lock in prices in just one state. Conversely, a company dealing with a multistate energy provider might lock in a fixed price for all its locations, even if rates vary from state to state.

Hedging relies on careful market projections. In 2006 a European paper manufacturer told Summit it wanted to avoid what had happened the previous year, when the rising cost of energy had cut into profits. The company wanted to lock in prices for a type of crude oil, because the price would bear on its costs for manufacturing and transportation. Oil was at $67 per barrel and projected by some analysts to go to $100. Summit decided, however, that the price was likely to fall, and it convinced the client to sign a short-term contract instead of locking in the rate for all of 2007. Indeed, prices fell sharply.

Another question to consider is how easily a company can pass the fluctuating costs along, says Tim Statts, vice president for risk management at Summit. It may be relatively easy to link the price of building materials, say, to the cost of producing them. Owens Corning, a maker of building materials, raises the price it charges consumers for asphalt when the cost of crude petroleum goes up. But it’s harder for a consumer products company to vary the price of a product like toothpaste.

Yet even Owens Corning, where energy accounts for 10 to 11 percent of annual costs, wants to smooth out the price fluctuations by hedging. Dave Andres, the company’s global leader for energy and precious metals, doesn’t try to time the markets in hopes of keeping energy costs to a bare minimum. Instead, he regularly signs contracts to buy a percentage of the company’s energy at fixed prices. That may mean paying too much sometimes and saving a lot at other times, but it cuts the variation in what he pays roughly in half, he says. Most of Owens Cornings’s energy comes from natural gas, and the company keeps an eye on crude oil as well. It is also considering strategies for hedging diesel, which is a big part of most large manufacturers’ transportation costs.

Andres points out that for all the benefits of hedging, the company’s main approach to reducing its risk is an effort to cut its energy use by 25 percent. “Our view,” he says, “is that the best hedge is that kilowatt you don’t use.”

Neil Savage (www.neilsavage.com) is a freelance writer based in Lowell, Massachusetts. He has written for IEEE Spectrum, Discover, and Nature Photonics.