Can We Build Tomorrow’s Breakthroughs?

Manufacturing in the United States is in trouble. That’s bad news not just for the country’s economy but for the future of innovation.

In a hangarlike building where General Electric once assembled steam turbines, a $100 million battery manufacturing facility is being constructed to make products using a chemistry never before commercialized on such a large scale. The sodium–metal halide batteries it will produce have been tested and optimized over the last few years by a team of materials scientists and engineers at GE’s sprawling research center just a few miles away. Now some of the same researchers are responsible for reproducing those results in a production facility large enough to hold three and a half football fields.

The engineers have moved from the bucolic research center, which sits on a hill overlooking the Mohawk River, down to the manufacturing site, which abuts the river at the edge of Schenectady, New York, a working-class town known in its heyday as Electric City. There, they supervise the installation and testing of robotics, high-temperature kilns, and analytic equipment that will monitor the production process. The new batteries use an advanced ceramic as an electrolyte inside a sealed metal case containing nickel chloride and sodium; the technology promises to store three times as much energy as the lead-acid batteries used in data centers, in heavy-duty electric vehicles, and for backup power. But almost anything can go wrong. If, say, the particles that make up the ceramic are uneven in size or haven’t been properly dried, battery performance could fall short. That means the conditions in the huge factory must be tightly controlled, and multi-ton devices must be able to match the exactness of lab equipment. “It’s not for the weak of heart,” says Michael Idelchik, GE’s vice president of advanced technologies.

The GE plant is one of a number of facilities around the country producing new technologies for rapidly growing markets in advanced batteries, electric vehicles, and solar power—but those efforts cannot counter the reality that the U.S. manufacturing sector is in trouble. After decades of outsourcing production in an effort to lower costs, many large companies have lost the expertise for the complex engineering and design tasks necessary to scale up and produce today’s most innovative new technologies, not to mention the appetite for the risks involved.

If you believe Thomas Friedman’s assertion that “the world is flat,” and that moving manufacturing to places where production is cheap makes companies more competitive, such a shift might not matter beyond its implications for the U.S. economy and its workers. But the United States remains the world’s most prolific source of new technologies, particularly materials-based ones, and evidence is growing that its diminished manufacturing capabilities could severely cripple global innovation. There are ample reasons to believe that the model of the U.S. computer industry—which has successfully outsourced much of its production in the last few decades and made design, not manufacturing, its priority—will not work effectively for companies trying to commercialize innovations in energy, advanced materials, and other emerging sectors.

Academic researchers have begun documenting the complex connections between innovation and manufacturing with an eye to clarifying how the loss of U.S. manufacturing could affect the emergence of new technologies. Willy Shih, a professor of management at Harvard Business School, has created a list of basic technologies in which the United States has squandered its lead in manufacturing in recent years. They include crystalline silicon wafers, LCDs, power semiconductors for solar cells, and many types of advanced batteries. And he has detailed how losing the “industrial commons”—the research know-how, engineering skills, and manufacturing expertise needed to make a specific technology—can often mean losing the knowledge and incentives to create advances in related technologies. For example, as silicon semiconductor production and associated supply chains have shifted to Asia, the development of new siliconbased solar cells has been hampered in the United States.

It turns out it’s not necessarily true that innovative technologies will simply be manufactured elsewhere if it doesn’t happen in the United States. According to research by Erica Fuchs, an assistant professor at Carnegie Mellon University, the development of integrated photonics, in which lasers and modulators are squeezed onto a single chip, has been largely abandoned by optoelectronic manufacturers as they have moved production away from the United States. Many telecom firms were forced to seek lower-cost production in East Asia after the industry’s collapse in the early 2000s, and differences in manufacturing practices meant that producing integrated photonic chips was not economically viable in those countries. Thus a technology that once appeared to be just a few years away from revolutionizing computers and even biosensors was forsaken. Economists might argue that we don’t care where something is produced, says Fuchs, but location can profoundly affect “the products that you choose to make and the technology trajectory itself.”

For many people in industry, the connections between innovation and manufacturing are a given—and a reason to worry. “We have learned that without a foothold in manufacturing, the ability to innovate is significantly compromised,” says GE’s Idelchik. The problem with outsourcing production is not just that you eventually lose your engineering expertise but that “businesses become dependent on someone else’s innovation for next-generation products.” One repercussion, he says, is that researchers and engineers lose their understanding of the manufacturing process and what it can do: “You can design anything you want, but if no one can manufacture it, who cares?”

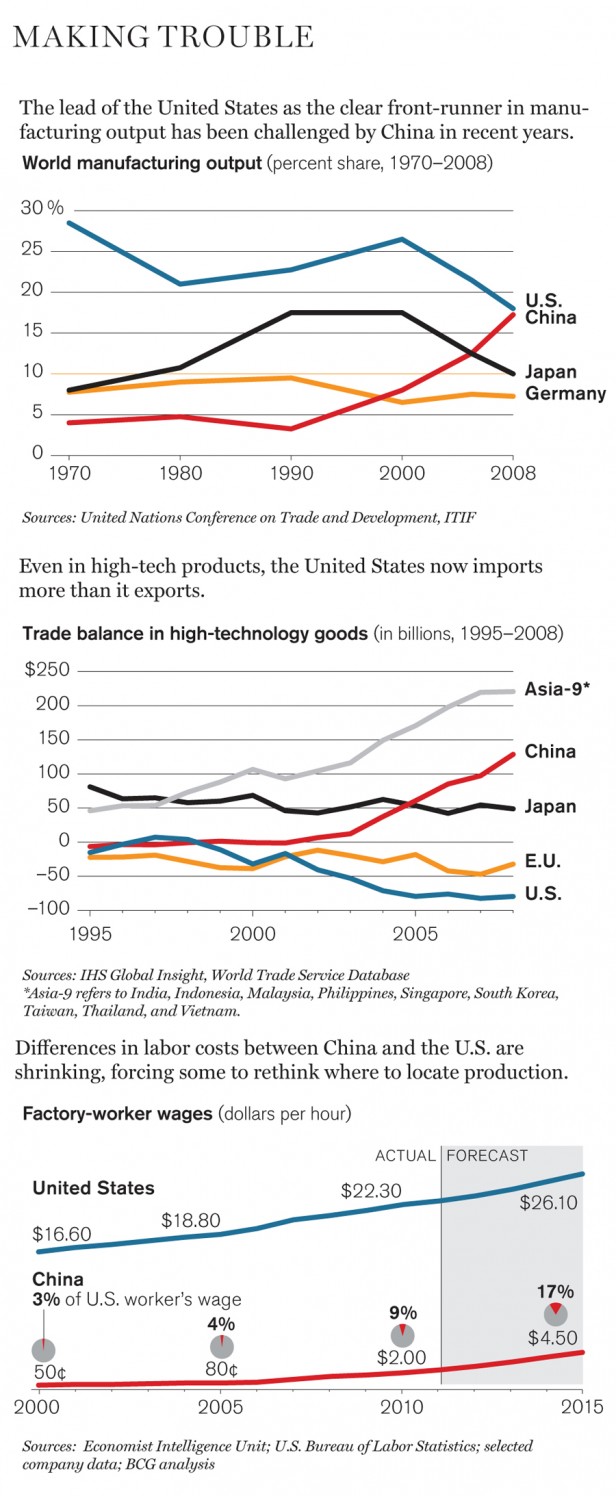

After decades as the world’s largest manufacturer, the United States now makes, according to some recent estimates, 19.4 percent of the world’s manufactured goods—second to China, which makes 19.8 percent. Even in high-tech products, the United States now imports more than it makes. Those statistics have implications for employment, national competitiveness, and even the politics and social structure of the country. But equally worrisome, especially over the long term, is what the declining ability of the United States to make stuff implies for the next generation of technology. Can the United States regain its ability to take on high-risk manufacturing? To ask the same question in a different way, are many of today’s most promising innovations in danger of suffering the same fate as integrated photonic chips? Can the United States regain its ability to take on high-risk manufacturing? To ask the same question in a different way, are many of today’s most promising innovations in danger of suffering the same fate as integrated photonic chips?

The city of Detroit, for decades the center of U.S. auto manufacturing, likes to tout its efforts at urban renewal. A modern baseball stadium sits at the edge of downtown; a bustling theater district is nearby. Yet empty and gutted skyscrapers are within walking distance of the shiny glass towers of General Motors’ headquarters and the new condos that rise above the city’s riverfront. And on the outskirts of the city, in areas bisected by highways with names such as Chrysler Freeway and Edsel Ford Freeway, the devastation is even more evident in the seemingly endless stretches of abandoned industrial buildings. Some 22 percent of the jobs in Michigan are still tied to automotive manufacturing, and a decade of bankruptcies and plunging sales among Detroit automakers has left the region reeling. Nearly a half million jobs have been lost in southeast Michigan since 2000.

Amid the ruins, however, the GM Detroit Hamtramck assembly plant is an oasis of order and activity. Though its parking lot is less than half full on a day in early fall, the massive plant, built in the mid-1980s to make Cadillacs and Buicks, embodies Detroit’s attempt to reinvent itself. A field of solar panels has been installed in front of it; at the edge of the visitors’ parking lot is a row of carports equipped with electrical outlets.

Inside the plant, Cadillacs and Buicks have been replaced on the assembly line by the Chevrolet Volt, GM’s recently introduced electric car, and its European counterpart, the Opel Ampera. The electric vehicles fill roughly every other available space on the production line, but GM hopes to ramp up production to 60,000 electric cars by next year. Like any modern auto manufacturing plant, the Detroit Hamtramck facility is a whirl of robotics and large parts moving deliberately along assembly lines that merge at critical points; at one of those intersections, the painted steel frame is slowly dropped down on the chassis and engine. Automated pneumatic wrenches puncture the relative quiet as they apply precise torque to bolt the pieces together.

Near the center of all the activity, sitting by themselves, are the T-shaped lithium-ion batteries that are the heart of the new car and a source of economic hope for much of Michigan. The 435-pound battery pack is a vast improvement over the hulking, 1,100-pound lead-acid batteries used in the ill-fated first generation of electric cars that GM made in the 1990s. The smaller, lighter new batteries are far easier to accommodate in a compact car like the Volt, and the new chemistry improves the vehicle’s performance.

Each battery pack contains some 288 cells, each of which contains a series of precisely matched thin sheets of anodes and cathodes. If GM makes 60,000 Volts next year, those cars would easily consume the output of several huge battery manufacturing plants. But if the electric-car market suddenly takes off—say, because of cheaper or more efficient batteries—the need could be far greater. It’s been estimated that if electric cars accounted for a tenth of U.S. auto sales, 43 large battery factories would be required to supply the automakers.

The potential appetite for batteries among GM and other automakers has led to the construction of at least half a dozen manufacturing and assembly plants in a 200-mile radius around Detroit. Spurred in part by the Obama administration’s $2.4 billion in funding for advanced-battery production and electric vehicles, this development presents a vision of what a recovery in the region’s manufacturing base might look like. It also presents a snapshot of the huge challenge involved in creating such an infrastructure.

About 125 miles north of the Detroit Hamtramck assembly plant is one of the largest of the new battery facilities. Dow Kokam, a joint venture of Dow Chemical, TK Advanced Battery, and the French firm Groupe Industriel Marcel Dassault, is building a $322 million factory in Midland, Michigan, that will be able to make enough lithium-ion battery cells for some 30,000 electric cars. Though construction is ongoing and much of the equipment is still being installed, a quick tour gives a sense of the operation’s size and complexity. In one large high-ceilinged room are a vast number of automated racks where each battery cell will be “formed,” a critical operation in which the battery is charged and discharged to precisely set the chemistry.

It’s this kind of scale and attention to detail that attract the interest of companies like Dow, the world’s second-largest chemical producer. The plant sits just outside the boundaries of Dow’s Michigan chemical operations, a small city of low-rise production buildings connected by a maze of crisscrossing overhead pipes. It’s a sprawling testimony to the connections between various ingredients and feedstocks used in making industrial products, and to the efficiencies of scale often required in manufacturing.

The supply chain for lithium-ion battery manufacturing starts deep within the chemical complex. Somewhere down one of the streets that run through the plant is a nondescript building where workers once made chemicals used in plastics. Now Dow is turning it into a production facility for the cathode and anode materials needed in lithium-ion batteries. Anyone who enters must don a white coat, wrap shoes in paper coverings, and submit to an air-spray shower designed to remove stray dust and particles. Inside, the powders for the cathodes and anodes are processed in large containers designed to minimize contamination. The materials will be shipped to one of the battery plants being built; though the nearby Dow Kokam plant is not obligated to buy the anodes and cathodes from its parent company, it would be a natural fit.

Like GE’s Idelchik, Dow’s chief technology officer, William Banholzer, acknowledges the risks of scaling up new technologies. But he says Dow’s size and deep pockets allow it to take risks that would be difficult for small startups, and its extensive infrastructure allows it to efficiently integrate the various aspects of the manufacturing process. Dow’s size also allowed it to hedge its bets on batteries by entering other new energy markets. On the opposite side of the vast manufacturing complex from the Dow Kokam plant, it is building a solar manufacturing facility, which will make roofing shingles that incorporate thin-film photovoltaics. “The scale of energy is so big it’s very tough to say energy is going to get solved by small companies,” says Banholzer. It’s not until you’ve actually begun manufacturing that you “get a look at your true costs and warts,” he says. In energy businesses where a demonstration plant might cost $500 million, “the venture-capital model breaks down,” he adds. “The big question is: can small companies ever compete with big companies in this area?”

SURVIVAL INSTINCTS

It is a question that gets at one of the key challenges involved in reviving the manufacturing sector. Banholzer is surely correct that startups cannot compete with the production capacity of a Dow or GE. But it also true that small companies are working on some of our most promising technologies, especially at the intersection of new materials and energy. If those technologies can be produced economically, they could greatly expand existing markets. The challenge for the startups, then, is to figure out a way to make their technologies using current manufacturing know-how while developing products that are radical enough to disrupt established technologies.

Ann Marie Sastry clearly thinks her startup can do just that. Housed in a small industrial park in Ann Arbor, Michigan, Sakti3 is working on a next-generation technology for solid-state batteries (see TR10, May/June 2011). The fabrication area in the back of the offices is strictly off limits to visitors, as are cameras and questions during a quick tour of the testing and design areas; CEO Sastry will reveal few details about the technology except to say that the battery has no liquid electrolytes and the company is using manufacturing equipment that was once employed to make potato-chip bags. But she is more forthcoming in explaining how the startup can thrive in the highly competitive advanced-battery sector.

The strategy begins with the recognition that any new technology must promise advantages far beyond what is possible with existing products. “If you start with the current [lithium-ion] technology,” she says, “you may get five or 10 or 20 points’ worth of performance by tweaking that process, but you have to accept that you’re never going to get anything transformative.” But doubling the energy density of batteries could have an enormous impact in powering communication devices, she says, especially in areas with little access to electricity for frequent charging. Transportation could be affected even more profoundly. New batteries with greater energy density and significantly lower cost could raise demand for electric vehicles to a whole new level, she says.

So she and her colleagues “started with the periodic table” to invent a new battery. From the first, the company knew the technology had to scale. “We didn’t take a clean sheet of paper to manufacturing,” she says. “We started by an analysis of manufacturing approaches that had been and could be scaled.”

Looking to the periodic table for materials that might overturn current technology is a frequent strategy these days for early-stage energy startups. Gerbrand Ceder, a materials scientist at MIT, initiated a “materials genome project” several years ago that uses computers to analyze and predict the properties of materials “across the known chemical universe” and hopes to create an open database of the information. (After the White House announced its Materials Genome Initiative, he agreed to rename his effort the Materials Project to avoid any confusion.) A major goal is to more efficiently identify materials that are suitable for manufacturing.

Ceder has systematically analyzed various compounds for their potential as battery materials. Using the computational tools developed by his materials genome project, Pellion, a startup in Cambridge, Massachusetts, that he cofounded in 2009, has identified new cathodes for a magnesium-based battery. If it works, Ceder says, the batteries could have double or triple the energy density of today’s lithium-ion batteries. Equally important, he says, they could “feed into the existing lithium-ion battery manufacturing.” And that’s critical, he says, because “if you have to invent a new material that can replace the existing one, it might take five to 10 years, but if you also have to invent a new design, it can take 10 to 20 years.”

Other promising early-stage energy startups are based on efforts to circumvent well-known manufacturing limitations. For example, Alta Devices, a company in Santa Clara, California, whose founders include leading researchers from Caltech and the University of California, Berkeley, is developing a way to make photovoltaic cells using films of gallium arsenide that are only a micrometer thick. Gallium arsenide, which is widely used as an ingredient in lasers and other photonic devices, has great optical properties but is too expensive for most solar cells. The new technology, however, uses so little of the material that its price is no longer prohibitive. Alta Devices has spent the last several years perfecting the production process; it has begun a pilot line to make the photovoltaic materials next year and hopes to start commercial production in 2013.

As the risks and cost of scaling up energy technologies grow increasingly evident, it’s becoming common for startups to consider the practicalities of manufacturing when they conceive their innovations. But how does a tiny company, even with a radically different material, hope to succeed in highly competitive solar and battery markets that require huge capital investments? Partnering with a large company is an obvious strategy. Alta Devices, for example, is working with Dow on next-generation materials for the chemical company’s solar shingles; GM is an investor in Sakti3. Still, the energy startups face the daunting truth that scaling up innovations into successful manufacturing operations can take hundreds of millions of dollars.

There is, however, at least one recent example of success.

LEARNING CURVE

When Yet-Ming Chiang cofounded A123 Systems in 2001 on the basis of his MIT research on battery materials, there was no advanced-battery manufacturing in the United States. Although much of the scientific work that led to the invention of lithium-ion batteries had been done in this country, including advances achieved at the University of Texas, it was Sony that commercialized the batteries in 1991. Subsequently, manufacturers in Korea and China made significant investments in the technology. With four times the energy capacity of nickel-cadmium batteries and twice that of newer nickel–metal hydride ones, lithium-ion batteries became the dominant technology in consumer devices, making today’s small, powerful cell phones and laptops possible.

Meanwhile, the two major U.S. battery producers, Duracell and Eveready (now called Energizer), tried to develop their own lithium-ion products during the 1990s. Eveready got as far as building a factory in Gainesville, Florida, but even as the plant prepared for commercial production, the price of lithium-ion batteries dropped and the company decided it was cheaper to buy cells from Japanese producers than to make its own. It exited the lithium-ion battery business, and Duracell soon followed.

So Chiang and his colleagues at A123 built a manufacturing plant in Changzhou, China (see “An Electrifying Startup,” May/June 2008). The move was meant not to outsource production, says Chiang, but to acquire the needed manufacturing know-how. Subsequently, A123 bought a South Korean manufacturer as a way to begin developing the expertise it needed to make the flat cells required for electric-car batteries. When A123 decided it needed to be closer to its potential automotive customers in Detroit, it cloned the Korean plant in Livonia, Michigan, and the Chinese factory a few miles away in Romulus, aided by a $249 million grant from the federal government. As a result of this strategy, A123 was able to become a major manufacturer in a remarkably short time, building the Livonia plant in just over a year and the Romulus plant in nine months.

The company soon became one of the nation’s highest-profile energy startups—and one of the few that have scaled up their technology, building what it claimed in 2010 was the “largest lithium-ion automotive battery plant in North America.” In 2009 it went public, raising around $400 million. But unfortunately for those hoping to emulate such success, the political and financial circumstances that allowed A123 to garner nearly $1 billion in private and public investments are long gone.

One of the lessons from A123 is “exactly how much it cost” to become successful, Chiang says. “And one wonders how often that can be replicated. In the current climate, one wonders whether there is a will to do this over and over again.” In the biotech industry, the path to commercialization has become clear over the years—partnering with large pharmaceutical companies, meeting expected milestones, and undergoing the regulatory approval process required for new products. But it’s not so simple for energy startups, says Chiang, whose latest startup, 24M, is hoping to develop a radically new battery technology. Those small companies developing new energy technologies, he says, “still have to figure it out.”

TEAM SPORTS

These days, Evergreen Solar’s three-year-old manufacturing plant in Marlborough, Massachusetts, sits empty with a large “For Lease” sign in front. The bankruptcy of Evergreen in August, and of Solyndra a month later, produced much hand-wringing over the future of solar power. In particular, the collapse of Solyndra, a Silicon Valley–based manufacturer that had received a $535 million loan guarantee from the federal government, has led to criticism of the role the government has played in supporting renewable energy and, in particular, its poor record in “picking winners.”

The government does have a record of backing some notorious energy failures. And scaling up new technologies is, of course, risky. But such criticisms have overshadowed the arguably more interesting lessons that can be gleaned from the bankruptcies: in many ways, the companies’ failures of both strategy and execution were manufacturing failures. Their business models depended on using radically new technologies to bring down the cost of making solar panels, ignoring the truism that new technologies are initially almost never cheaper than well-optimized existing processes. And neither company had products innovative enough to induce most customers to pay a premium price. Evergreen and Solyndra faced many unexpected market changes—among them a sudden drop in silicon prices and the overproduction of solar panels—but the ability of competing companies to continue lowering their manufacturing costs for more conventional solar panels shouldn’t have been a surprise (see “The Chinese Solar Machine”).

There are other manufacturing lessons to be learned from the collapses of these two businesses. Evergreen’s innovation revolved around a single step in the production process—a way to make silicon wafers more cheaply. Yet the company made and sold complete solar panels—and they were a different size from the industry standard, forcing its customers into the undesirable position of making a long-term commitment to a specific technology.

Likewise, Solyndra (one of TR’s 50 most innovative companies in 2010) made a series of manufacturing missteps. In a filing with government regulators in December 2009, the company acknowledged that “our custom-built equipment may take longer and cost more to engineer and build than expected and may never operate as required to meet our production plans.” Such words of caution are often boilerplate in these filings, but in this case they were prescient. In particular, Solyndra attempted to build out its manufacturing capacity at a rapid pace, planning a second production plant even as it was still expanding the first one—and losing vast amounts of money because of its relatively high costs. In retrospect, it is obvious that both companies expanded manufacturing far too fast, with far too little understanding of their unique production processes, their competition, or their customers’ requirements.

A way to avoid such mistakes is to increase collaboration among companies developing new technologies. The outskirts of Albany will never be confused with Silicon Valley, but the names of the companies at the College of Nanoscale Science and Engineering there are familiar to anyone in the semiconductor industry: Intel, IBM, TSMC, Applied Materials, and Tokyo Electron. The idea is that the shared facilities provide an opportunity for chip makers, equipment suppliers, and engineering companies to develop and evaluate their products. Last year Sematech, the U.S. consortium of semiconductor companies, moved its operations to the $12 billion complex. Its newest initiative: to help revive the U.S. solar industry the same way it helped the semiconductor industry regain its footing in the 1980s and 1990s.

One of the lessons of the Solyndra failure is that it involved “betting on a very risky technology” and spending hundreds of millions on unproven production processes, says Pradeep Haldar, who leads the new Photovoltaic Manufacturing Consortium in Albany, a partnership between Sematech and CNSE. In contrast, he says, manufacturers of thin-film solar cells can use the existing infrastructure at the Albany facility to get “a reality check,” including reactions from materials suppliers and potential customers.

This collaborative approach is attractive even for large manufacturers such as GE. “Innovation is a team sport,” says Idelchik, but too often in the United States “we’re trying to do it in a vacuum.” Opportunities like those offered at the Albany nanotech center are particularly important, he believes, because manufacturers are in a period of transition. The worldwide recession that began in 2008 left companies with vast amounts of overcapacity, but costs for materials and labor have continued to rise along with the standard of living in countries such as China and India. This means it’s no longer effective to try to squeeze cost out of manufacturing by, for example, chasing lower-priced labor. To stay competitive, Idelchik says, companies need to move to “high-risk, high-payoff” manufacturing of advanced products and materials. However, he adds, such high-risk manufacturing requires an “ecosystem” of suppliers, equipment makers, and customers.

That ecosystem is essentially what Harvard’s Willy Shih calls the “industrial commons.” However it’s described, it is what the United States has lost in LCDs and integrated photonics, has nearly lost in advanced batteries, and is rapidly losing in silicon solar panels. It is what A123 and Dow are attempting to help rebuild for advanced batteries in Michigan, what Sematech hopes to initiate for thin-film solar panels, and what startups like Pellion, 24M, and Alta Devices all hope they can leverage—and then eventually disrupt.

Whether such startups survive will depend, ironically, very much on whether the markets they ultimately hope to replace are robust and growing. Yet the industrial commons are fragile, and their survival will depend both on markets and on government policies. The birth of advanced-battery manufacturing in Michigan is largely a result of support from the Obama administration. Whether it thrives will depend on how many electric cars GM and others are able to sell and whether the government continues to provide incentives for the fledgling industry, including funding for research. In the longer term, its health may very well depend on how well it is able to adopt truly innovative new technologies from the early-stage startups. The consequences will be felt deeply. As Shih has demonstrated, the United States has lost key manufacturing sectors and related innovation skills multiple times. And his list of today’s at-risk technologies is long. If advanced batteries, solar technologies, and manufacturing of advanced materials become yet more casualties, it will surely damage the ability to invent future technologies.

These days Yet-Ming Chiang is spending at least part of his hectic schedule among the cramped cubicles of 24M, a five-minute bike ride from his MIT labs. About three years ago, while working at A123 on a sabbatical from MIT, Chiang began thinking about what the next generation of battery technology might look like. Much of the expense of manufacturing lithium-ion batteries is due to various non-active components and the multistep process of layering the electrodes and cathodes. The actual energy-storing parts—the electrodes and electrolyte—account for roughly a fifth of the total cost. What if, he wondered, you could design a battery that got rid of the non-energy-storing ingredients and the expensive cell and module assembly? The result is the flow battery that 24M is developing, in which the electrodes circulate in a semisolid form. A potential benefit of this design is that manufacturing it could be much less capital-intensive. What’s more, says Chiang, it is designed to work with the existing supply chain and manufacturing infrastructure for lithium-ion batteries.

Chiang says his experience with A123 was critical in coming up with the new battery design. “The best way to do battery research is having started a battery company,” he says. “Being close to the manufacturing, you recognize what can have an impact. It is the argument for why manufacturing is so important in these developing areas.”

David Rotman is Technology Review’s editor.